State regulators shuttered a local bank in rural Texas last month citing “insider abuse and fraud by former officers,” breaking a string of 17 months without a bank failure.

Texas Banking Commissioner Charles G. Cooper called the closure of Enloe State Bank an “isolated case” in a recent interview. Other experts agree the May 31, 2019, failure does not foreshadow a return to Great Recession-era economic conditions, when hundreds of banks failed and millions of Americans lost their jobs.

“This appears to be idiosyncratic to the bank,” said Kevin Jacques, a former economist with the U.S. Department of the Treasury who teaches finance at Baldwin Wallace University. “If it had been the banking system, then what we would expect to see is a whole wide variety of failures either within an economic region or across the country.”

But the exact cause of the bank’s failure remains a mystery. State and federal regulators are investigating a suspicious fire that destroyed key documents two days before the bank’s officers were set to turn them over to the state for a routine examination of its books.

Burned files arouse suspicion

Enloe State Bank, founded in 1928 in Enloe, has maintained only one branch in nearby Cooper, Texas, since 2008.

Cooper has a population of just under 2,000, making it the largest city in Delta County. It’s a prairie town built around a red-brick cobblestone square that grew up around the cotton crop and the Texas Midland Railroad, both now defunct.

“For the past 82 years, Enloe State Bank has strived to provide strength and stability to the small communities in which it serves with unprecedented customer service,” read the bank’s website before it was replaced with a Federal Deposit Insurance Corp. closure notice last month.

Enloe State Bank’s trouble with regulators began in early May after an incident at the bank’s main offices in a squat brick building next to a Dairy Queen on Texas Highway 24, about 90 miles northeast of Dallas.

Delta County Sheriff Ricky Smith said in an interview that the bank’s cleaning crew called 911 after seeing smoke billowing from a window at about 6:30 p.m. on Saturday, May 11.

After firefighters extinguished the blaze, Smith said first responders found “several piles” of burned files on a conference room table. He said no employees were inside the bank at the time of the incident.

Regulators from the Texas Department of Banking were scheduled to visit the bank the following Monday to collect documents as part of a routine examination. Cooper, who heads the agency, said the bank had received a list of documents to prepare ahead of time.

“A lot of the files we requested were the documents that were burned,” Cooper said.

The Bureau of Alcohol, Tobacco, Firearms and Explosives and the FDIC are investigating the fire, which Smith deems “suspicious.”

A deeper inquiry after the fire revealed the bank was insolvent, said Cooper, who has been examining banks while working in the public and private sector since 1970.

‘A giant question mark’

State regulators then turned the bank over to the FDIC, which brokered the sale of all $30.8 million of its insured deposits to Bowie, Texas-based Legend Bank, N.A. About $500,000 exceeded FDIC insurance limits, according to the agency, meaning some customers must contact the agency directly to discuss their deposits.

The FDIC announced Enloe State Bank’s closure to the public with a Friday afternoon press release on May 31. By Monday, June 3, Legend had the Cooper branch reopened, staffed by the same tellers.

Customers had no interruption in accessing banking services over the weekend, according to the FDIC and Legend Bank.

In the deal, Legend Bank also purchased about 14% of the failed bank’s $36.7 million in assets — which could include cash, loans, securities and physical assets. The FDIC estimates the failure will cost its Deposit Insurance Fund, composed of premiums paid by banks, about $27 million.

For such a small community bank, such a large hit to the FDIC’s insurance fund caught the eye of Nate Tobik, CEO of CompleteBankData.com and author of “The Bank Investor’s Handbook,” who dug into lending data to paint a clearer picture of Enloe State Bank’s failure.

Enloe State Bank was classified as agriculturally focused, and Tobik examined the bank’s $10 million in loans to finance agricultural production. But when he cross-referenced borrowers who own larger plots of land with lists of farmers who have received government subsidies — available for all but the smallest farming operations —he came up empty-handed.

“If the people you’re lending to aren’t receiving subsidies, they aren’t even farmers of note,” he said. “Where did that $10 million go?”

“That’s a giant question mark.,” Tobik continued.

Tobik likens cases of fraud of this scale to a bank deciding to give a $50,000 loan to someone offering a nearly worthless 1992 Honda Civic as collateral.

Generally in these situations, “they’re loaning to businesses with inflated revenues, or inflated income, inflated asset values, and the underlying collateral or cash flows aren’t there to support what those loans were made against,” Tobik said.

Cooper declined to go into further detail about the fraud uncovered at Enloe State Bank. Speaking generally about cases of this nature, he said the Texas Department of Banking and FDIC will investigate and will refer their findings to the FBI or the U.S. Attorney’s Office.

Cooper could not provide a timeline for the Texas Department of Banking and FDIC investigations, but said, “usually, things of this nature are dealt with fairly quickly.”

A Legend spokesperson referred specific inquiries about its acquisition of Enloe State Bank to a Texas Department of Banking press release.

Seventeen months ago

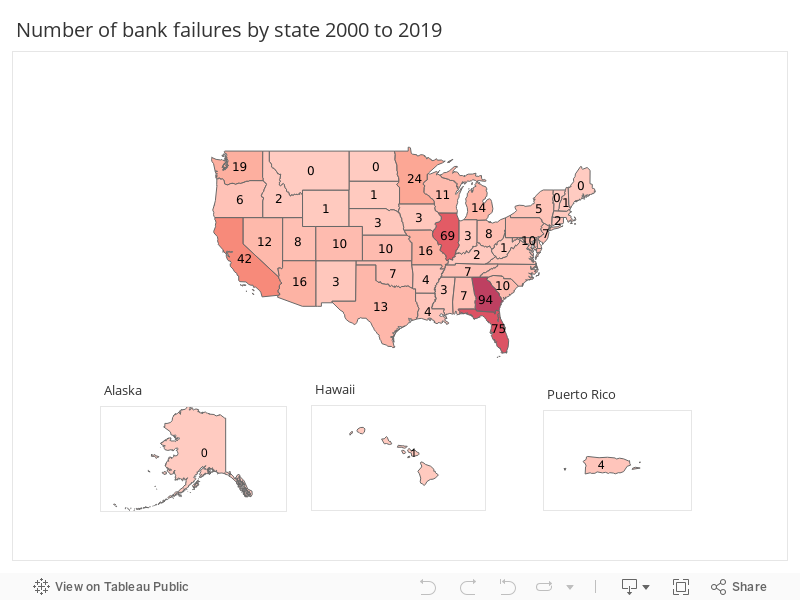

Only three times since the FDIC’s founding in 1933 has the U.S. gone a full calendar year without a bank failure; 2018 was one such year. So were 2005 and 2006, the lead up to the financial crisis.

Enloe State Bank’s failure snapped a 17-month streak without a failure.

For Anat Admati, professor of finance and economics at Stanford University’s Graduate School of Business, long stretches without failures don’t mean a healthy banking sector.

“My feeling is that banks are living dangerously in general,” Admati said.

Admati has co-authored a book called “The Bankers’ New Clothes,” criticizing banks’ excessive reliance on government-subsidized borrowing to fund their investments, which in her view makes the banking system dangerously fragile. Higher equity requirements should be imposed, she wrote in the book, making for a healthier mix of debt and equity in banks’ funding.

But Admati said the particulars often vary in individual cases of bank failure, and there is always the potential for financial abuse by officers.

“Banks are interesting, because obviously, as their robber said when asked, ‘Why did you rob the bank?’ he said, ‘That’s where the money is,’” Admati said.

The last bank to fail, in December 2017, Washington Federal Bank for Savings in Bridgeport, Illinois, remains under investigation by federal regulators, but an audit revealed examiners missed “red-flags” that should have raised suspicions earlier.

One of the bank’s managers tipped off federal Treasury Department officials about issues there.

“The manager disclosed that she had been informed by a bank employee that the employee and the bank’s then-president had been regularly falsifying loan payments for at least 29 loans totaling approximately $68 million in aggregate assets — and had falsified Washington Federal’s loan trial balance before providing it to examiners,” according to the audit report by the Treasury Department’s Office of Inspector General.

Five days after the manager alerted regulators, the bank’s president and CEO John Gembara hanged himself at the home of a friend and one of the bank’s longtime customers, according to the Cook County medical examiner’s office.

As of Sept. 30, 2018, the FDIC estimated that the failure in 2017 of Washington Federal Bank for Savings in Bridgeport, Illinois, cost $82.6 million to its Deposit Insurance Fund.

The audit report noted that the bank “was perceived as a ‘training’ or ‘practice’ bank for new Treasury Department examiners because of “the perception that Washington Federal was a non-complex bank with a low-risk profile” — a major factor in the fraud going undetected for years, according to the report.

As of Sept. 30, 2018, the FDIC estimated the bank’s failure cost $82.6 million to its Deposit Insurance Fund.

Since then, the FDIC has sued Bansley and Kiener, a Chicago-based accounting firm that gave Washington Federal a clean bill of health in an audit several months before regulators closed the bank, to compel the firm to turn over documents pertaining to the bank.

The Chicago Sun-Times has reported that regulators have identified $14.5 million in unsecured “loan advances” given by Gembara to four Washington Federal customers, including the owner of the home where Gembara was found dead, without adequate documentation.

In efforts to recoup debts to the bank, officials have been unable to locate a 46-foot yacht owned by Gembara named Expelliarmus, in reference to the disarming spell from the Harry Potter books, according to the Sun-Times.

‘Fraud and insider abuse’ at Enloe State Bank

The exact circumstances of Enloe State Bank’s fraud case remain cloudy, including how far back in time it stretches.

“A bank can remain insolvent for a long time,” Admati said. “It could pretend to be better than it is for longer than other companies in the economy.”

A holding company called Entex Bancshares Inc. controlled Enloe State Bank from 1983 until its closure in May. The Investigative Reporting Workshop contacted six former Entex board members.

Joe Turner, 92, of Fort Worth, who was last listed as a member of the board of directors on 2017 Texas corporation records, said he had not been in contact with other directors, was unaware of any wrongdoing at the bank and had not been notified of its closure.

“I don’t know much about it,” Turner said.

Patricia Smith Thatcher, 71, who was listed as a member of the Entex board of directors on an annual report filed in September 2018 with the Federal Reserve, and Charles L. Thatcher Jr., 74, who was listed as a shareholder, not a director, referred questions about the bank to a lawyer, James R. Rodgers with The Moore Law Firm, L.L.P. in Paris, Texas.

In a phone interview, Rodgers referred questions about the reason for the bank’s closure to the FDIC, referencing “allegations against the former president of the bank and possibly another bank officer.”

Anita Moody, 56, Enloe State Bank president, did not return several calls and emails seeking comment. Moody also was listed as a member of the Entex board of directors.

Other former Entex directors could not be reached via phone numbers listed as theirs on public records.

Rodgers said he represented the board of the directors of Enloe State Bank, not Entex, for the last several weeks of the bank’s existence. That board included Charles Thatcher Jr., Johnny Patterson, 66, Fred Wilkerson, 75, and Sam Bettes, Rodgers said.

“They’re all very honest and reasonable people who were not aware of any wrongdoing,” Rodgers said.

This story has been updated to clarify Admati’s work.

Follow the health of banks and credit unions nationwide with our BankTracker project.